Considering a purchasing or selling a property in Paradise Valley? Call Joe and Linda Szabo – The Real Estate Experts!

We hope that you enjoy reading and analyzing the Paradise Valley Luxury Home Report and should you have any questions or comments, please feel free to Contact Joe Szabo at 480.688.2020 or email him directly at Joe@ScottsdaleRealEstateTeam.com or Joe@AZLuxuryHomes.com. You can also visit https://www.AZLuxuryHomes.com or https://scottsdalerealestateteam.com to find out more about Paradise Valley Homes for Sale and Estates for Sale in Paradise Valley and to search the Paradise Valley MLS for Scottsdale Home Listings.

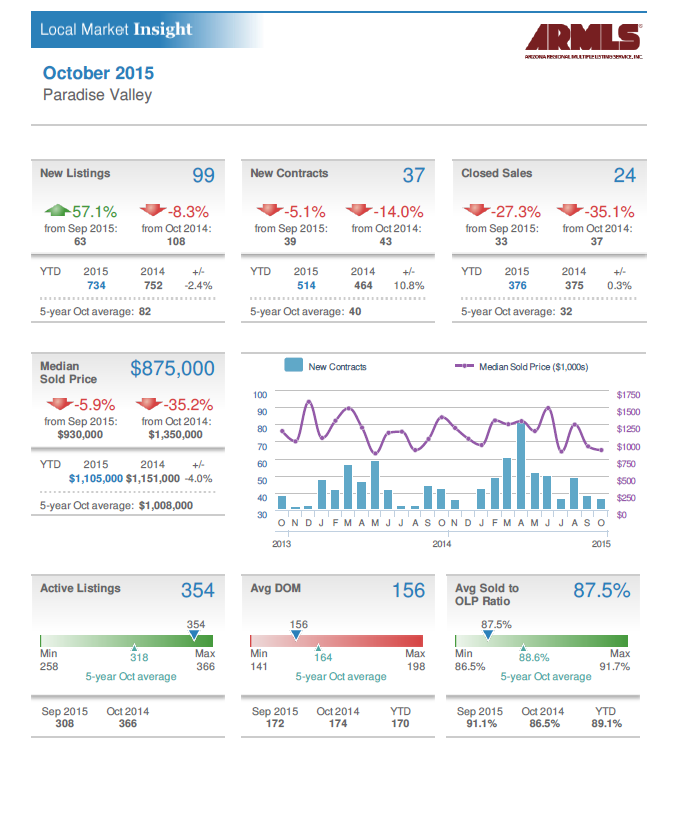

Please note that this Paradise Valley Real Estate Blog is for informational purposes and not intended to take the place of a licensed Paradise Valley Real Estate Agent. The Szabo Group offers first class real estate services to clients in the Scottsdale and Paradise Valley Greater Phoenix Metropolitan Area in the buying and selling of Luxury homes in Arizona & the real estate market . Award winning Realtors and Re/MAX top producers and best real estate agent for Luxury Homes in Paradise Valley, The Szabo group delivers experience, knowledge, dedication and proven results.

Considering a purchasing or selling a property in Paradise Valley? Call Joe and Linda Szabo – The Real Estate Experts!

We hope that you enjoy reading and analyzing the Paradise Valley Luxury Home Report and should you have any questions or comments, please feel free to Contact Joe Szabo at 480.688.2020 or email him directly at Joe@ScottsdaleRealEstateTeam.com or Joe@AZLuxuryHomes.com. You can also visit https://www.AZLuxuryHomes.com or https://scottsdalerealestateteam.com to find out more about Paradise Valley Homes for Sale and Estates for Sale in Paradise Valley and to search the Paradise Valley MLS for Scottsdale Home Listings.

Please note that this Paradise Valley Real Estate Blog is for informational purposes and not intended to take the place of a licensed Paradise Valley Real Estate Agent. The Szabo Group offers first class real estate services to clients in the Scottsdale and Paradise Valley Greater Phoenix Metropolitan Area in the buying and selling of Luxury homes in Arizona & the real estate market . Award winning Realtors and Re/MAX top producers and best real estate agent for Luxury Homes in Paradise Valley, The Szabo group delivers experience, knowledge, dedication and proven results.

People used to get there with second jobs, but lenders don’t see this as much since the recession.

“Instead, what you see is somebody graduates from college, they move back home to pay off debt and save money, and they work 50, 60 hours a week at the job that they found,” said Staci Titsworth, a regional manager for PNC Mortgage in Pittsburgh.

There are also more double-income households, and more first-time buyers waiting to buy homes where they can stay more than 5 years and possibly raise families, she said.

People are also coming in below 20 percent, which typically requires paying mortgage insurance.

Even with mortgage insurance tacked on, people tend to have lower monthly payments for mortgages than for rent. Indeed, homeowners in general can expect to spend about 15 percent of their monthly income on mortgage payments (without mortgage insurance) for a median-valued home, while renters can expect to spend 30 percent on rent.

Borrowers in pricey markets have taken the lower down payment route for years.

That’s how Sara Clarke, an editor at U.S. News & World Report, and her husband landed their first home: a townhouse in Alexandria, VA, that cost $299,500. They put down 5 percent, money saved from a childhood paper route and fast-food jobs, plus a little help from a relative.

By the time they sold it about 10 years later, they had accrued the 20 percent down payment they needed for a single-family home in Fairfax County. They even had money left over to replenish a savings account depleted by upgrades on their first kitchen, bathrooms, roof and “redoing everything we could redo.”

Assistance from parents remains a common way to get a foot in the door of your own home. Loans and gifts from family and friends rose from 8 percent to 21 percent during the recession, and was down to 13 percent last year.

JPMorgan Chase has also seen first-time buyers becoming more disciplined about spending and tapping into 401(k)s, said Sean Grzebin, the bank’s head of retail mortgage lending.

Check out Zillow Research for more on down payments, rents and the housing market in general.

People used to get there with second jobs, but lenders don’t see this as much since the recession.

“Instead, what you see is somebody graduates from college, they move back home to pay off debt and save money, and they work 50, 60 hours a week at the job that they found,” said Staci Titsworth, a regional manager for PNC Mortgage in Pittsburgh.

There are also more double-income households, and more first-time buyers waiting to buy homes where they can stay more than 5 years and possibly raise families, she said.

People are also coming in below 20 percent, which typically requires paying mortgage insurance.

Even with mortgage insurance tacked on, people tend to have lower monthly payments for mortgages than for rent. Indeed, homeowners in general can expect to spend about 15 percent of their monthly income on mortgage payments (without mortgage insurance) for a median-valued home, while renters can expect to spend 30 percent on rent.

Borrowers in pricey markets have taken the lower down payment route for years.

That’s how Sara Clarke, an editor at U.S. News & World Report, and her husband landed their first home: a townhouse in Alexandria, VA, that cost $299,500. They put down 5 percent, money saved from a childhood paper route and fast-food jobs, plus a little help from a relative.

By the time they sold it about 10 years later, they had accrued the 20 percent down payment they needed for a single-family home in Fairfax County. They even had money left over to replenish a savings account depleted by upgrades on their first kitchen, bathrooms, roof and “redoing everything we could redo.”

Assistance from parents remains a common way to get a foot in the door of your own home. Loans and gifts from family and friends rose from 8 percent to 21 percent during the recession, and was down to 13 percent last year.

JPMorgan Chase has also seen first-time buyers becoming more disciplined about spending and tapping into 401(k)s, said Sean Grzebin, the bank’s head of retail mortgage lending.

Check out Zillow Research for more on down payments, rents and the housing market in general.