By Joe Szabo, Scottsdale Real Estate Team

Rates are up .5 percent so far in 2017, and could go higher. This raises the question of whether it makes sense to buy your rate down to control your mortgage costs. Let’s review the market outlook, then answer the question.

Where are rates headed from here?

Rates are tied to daily trading in mortgage bonds, and rates rise when bonds sell on improving economic sentiment — this has been happening in 2017.

Concurrently, the Federal Reserve controls short-term rates in the economy using overnight bank-to-bank lending rates. They hike these rates when they believe the economy is improving. Even though mortgage bonds represent longer-term rates, these Fed hikes still fuel selling of mortgage bonds, pushing mortgage rates higher.

The Fed began hiking rates in December, and has indicated continued hiking if economic data stays positive. Their next three rate policy meetings are March 15, May 3, and June 13.

Mortgage rates will rise as the Fed’s economic tone becomes more optimistic. The Mortgage Bankers Association calls for rates to rise about 1 percent in 2017 versus 2016, and we’ve only seen half of that so far.

With many signs pointing to higher rates, let’s address the rate buy down question.

What is buying down my rate?

“Buying your rate down” or “paying points” means you’re paying an extra fee on top of standard loan fees like appraisal, underwriting, and credit report to get a lower rate.

If you were getting a 30-year fixed loan of $325,000, you might get two options with and without points. Today the option with zero points might show the rate as 4.25 percent, and the option with 1 percent in points — equal to $3,250 — might show the rate as 4 percent.

Paying $3,250 at closing to lower your rate by .2 percent lowers your payment $42 per month, and lowers your interest cost $68 per month.

How do I calculate if I should buy my rate down?

To determine if you should buy down your rate, calculate how long it takes your monthly interest cost savings to repay the cost of the points. In our example, we divide the $3,250 you’re paying at closing by the $68 in monthly interest cost savings, showing it takes 48 months for the interest cost savings to repay the points.

If you’re going to live in the home longer than four years, then paying the points makes sense. Note, however, that it doesn’t make sense if you’re getting a 5-year ARM instead of a 30-year fixed — because the 5-year ARM would adjust to a higher payment just one year after you broke even on buying your rate down.

What are the dangers of buying down the rate?

Work with your lender to calculate how long it takes interest cost savings from paying points to repay the points. If you’re in the home (or the loan) longer than this breakeven timeline, you won’t lose money.

But if rates drop after you pay points, your risk is that you’d need to spend money on a refinance to keep you in the market, but that refinance cost could come during the time you’re still waiting to break even on the points you paid.

Given the rate projections noted above, that risk is low for now.

What if I need to buy down my rate to qualify?

Rising rates make your payment higher, which reduces your affordability.

Lenders allow you to spend up to 43 percent of your income on housing and non-housing bills each month. If rising rates don’t push you over this threshold and your budget is still manageable, you can proceed.

But if rising rates push you over this qualifying threshold, you don’t have to rely solely on buying your rate down to qualify.

You can also reduce your purchase price. Or if you don’t want to resort to that, the smartest way to qualify is to find other debt to trim.

How do I know if a rate buy down is being disclosed to me correctly?

Federal law requires lenders to give you a disclosure called a Loan Estimate within three days of a complete loan application.

The Loan Estimate’s second page shows Points in the top left section called Loan Costs. This will show the exact percentage of the loan amount for any points being quoted. It also shows the dollar amount of the points.

Please note that this Scottsdale Real Estate Blog is for informational purposes and not intended to take the place of a licensed Scottsdale Real Estate Agent. The Szabo Group offers first class real estate services to clients in the Scottsdale Greater Phoenix Metropolitan Area in the buying and selling of Luxury homes in Arizona. Award winning Realtors and Re/MAX top producers and best real estate agent for Luxury Homes in Scottsdale, The Szabo group delivers experience, knowledge, dedication and proven results. Contact Joe Szabo at 480.688.2020, info@ScottsdaleRealEstateTeam.com or visit www.scottsdalerealestateteam.com to find out more about Scottsdale Homes for Sale and Estates for Sale in Scottsdale and to search the Scottsdale MLS for Scottsdale Home Listings.

By Joe Szabo, Scottsdale Real Estate Team

Rates are up .5 percent so far in 2017, and could go higher. This raises the question of whether it makes sense to buy your rate down to control your mortgage costs. Let’s review the market outlook, then answer the question.

Where are rates headed from here?

Rates are tied to daily trading in mortgage bonds, and rates rise when bonds sell on improving economic sentiment — this has been happening in 2017.

Concurrently, the Federal Reserve controls short-term rates in the economy using overnight bank-to-bank lending rates. They hike these rates when they believe the economy is improving. Even though mortgage bonds represent longer-term rates, these Fed hikes still fuel selling of mortgage bonds, pushing mortgage rates higher.

The Fed began hiking rates in December, and has indicated continued hiking if economic data stays positive. Their next three rate policy meetings are March 15, May 3, and June 13.

Mortgage rates will rise as the Fed’s economic tone becomes more optimistic. The Mortgage Bankers Association calls for rates to rise about 1 percent in 2017 versus 2016, and we’ve only seen half of that so far.

With many signs pointing to higher rates, let’s address the rate buy down question.

What is buying down my rate?

“Buying your rate down” or “paying points” means you’re paying an extra fee on top of standard loan fees like appraisal, underwriting, and credit report to get a lower rate.

If you were getting a 30-year fixed loan of $325,000, you might get two options with and without points. Today the option with zero points might show the rate as 4.25 percent, and the option with 1 percent in points — equal to $3,250 — might show the rate as 4 percent.

Paying $3,250 at closing to lower your rate by .2 percent lowers your payment $42 per month, and lowers your interest cost $68 per month.

How do I calculate if I should buy my rate down?

To determine if you should buy down your rate, calculate how long it takes your monthly interest cost savings to repay the cost of the points. In our example, we divide the $3,250 you’re paying at closing by the $68 in monthly interest cost savings, showing it takes 48 months for the interest cost savings to repay the points.

If you’re going to live in the home longer than four years, then paying the points makes sense. Note, however, that it doesn’t make sense if you’re getting a 5-year ARM instead of a 30-year fixed — because the 5-year ARM would adjust to a higher payment just one year after you broke even on buying your rate down.

What are the dangers of buying down the rate?

Work with your lender to calculate how long it takes interest cost savings from paying points to repay the points. If you’re in the home (or the loan) longer than this breakeven timeline, you won’t lose money.

But if rates drop after you pay points, your risk is that you’d need to spend money on a refinance to keep you in the market, but that refinance cost could come during the time you’re still waiting to break even on the points you paid.

Given the rate projections noted above, that risk is low for now.

What if I need to buy down my rate to qualify?

Rising rates make your payment higher, which reduces your affordability.

Lenders allow you to spend up to 43 percent of your income on housing and non-housing bills each month. If rising rates don’t push you over this threshold and your budget is still manageable, you can proceed.

But if rising rates push you over this qualifying threshold, you don’t have to rely solely on buying your rate down to qualify.

You can also reduce your purchase price. Or if you don’t want to resort to that, the smartest way to qualify is to find other debt to trim.

How do I know if a rate buy down is being disclosed to me correctly?

Federal law requires lenders to give you a disclosure called a Loan Estimate within three days of a complete loan application.

The Loan Estimate’s second page shows Points in the top left section called Loan Costs. This will show the exact percentage of the loan amount for any points being quoted. It also shows the dollar amount of the points.

Please note that this Scottsdale Real Estate Blog is for informational purposes and not intended to take the place of a licensed Scottsdale Real Estate Agent. The Szabo Group offers first class real estate services to clients in the Scottsdale Greater Phoenix Metropolitan Area in the buying and selling of Luxury homes in Arizona. Award winning Realtors and Re/MAX top producers and best real estate agent for Luxury Homes in Scottsdale, The Szabo group delivers experience, knowledge, dedication and proven results. Contact Joe Szabo at 480.688.2020, info@ScottsdaleRealEstateTeam.com or visit www.scottsdalerealestateteam.com to find out more about Scottsdale Homes for Sale and Estates for Sale in Scottsdale and to search the Scottsdale MLS for Scottsdale Home Listings.Should I Buy Down My Rate After 2017 Fed Rate Hikes? By Joe Szabo, Scottsdale Real Estate Team

By Joe Szabo, Scottsdale Real Estate Team

Rates are up .5 percent so far in 2017, and could go higher. This raises the question of whether it makes sense to buy your rate down to control your mortgage costs. Let’s review the market outlook, then answer the question.

Where are rates headed from here?

Rates are tied to daily trading in mortgage bonds, and rates rise when bonds sell on improving economic sentiment — this has been happening in 2017.

Concurrently, the Federal Reserve controls short-term rates in the economy using overnight bank-to-bank lending rates. They hike these rates when they believe the economy is improving. Even though mortgage bonds represent longer-term rates, these Fed hikes still fuel selling of mortgage bonds, pushing mortgage rates higher.

The Fed began hiking rates in December, and has indicated continued hiking if economic data stays positive. Their next three rate policy meetings are March 15, May 3, and June 13.

Mortgage rates will rise as the Fed’s economic tone becomes more optimistic. The Mortgage Bankers Association calls for rates to rise about 1 percent in 2017 versus 2016, and we’ve only seen half of that so far.

With many signs pointing to higher rates, let’s address the rate buy down question.

What is buying down my rate?

“Buying your rate down” or “paying points” means you’re paying an extra fee on top of standard loan fees like appraisal, underwriting, and credit report to get a lower rate.

If you were getting a 30-year fixed loan of $325,000, you might get two options with and without points. Today the option with zero points might show the rate as 4.25 percent, and the option with 1 percent in points — equal to $3,250 — might show the rate as 4 percent.

Paying $3,250 at closing to lower your rate by .2 percent lowers your payment $42 per month, and lowers your interest cost $68 per month.

How do I calculate if I should buy my rate down?

To determine if you should buy down your rate, calculate how long it takes your monthly interest cost savings to repay the cost of the points. In our example, we divide the $3,250 you’re paying at closing by the $68 in monthly interest cost savings, showing it takes 48 months for the interest cost savings to repay the points.

If you’re going to live in the home longer than four years, then paying the points makes sense. Note, however, that it doesn’t make sense if you’re getting a 5-year ARM instead of a 30-year fixed — because the 5-year ARM would adjust to a higher payment just one year after you broke even on buying your rate down.

What are the dangers of buying down the rate?

Work with your lender to calculate how long it takes interest cost savings from paying points to repay the points. If you’re in the home (or the loan) longer than this breakeven timeline, you won’t lose money.

But if rates drop after you pay points, your risk is that you’d need to spend money on a refinance to keep you in the market, but that refinance cost could come during the time you’re still waiting to break even on the points you paid.

Given the rate projections noted above, that risk is low for now.

What if I need to buy down my rate to qualify?

Rising rates make your payment higher, which reduces your affordability.

Lenders allow you to spend up to 43 percent of your income on housing and non-housing bills each month. If rising rates don’t push you over this threshold and your budget is still manageable, you can proceed.

But if rising rates push you over this qualifying threshold, you don’t have to rely solely on buying your rate down to qualify.

You can also reduce your purchase price. Or if you don’t want to resort to that, the smartest way to qualify is to find other debt to trim.

How do I know if a rate buy down is being disclosed to me correctly?

Federal law requires lenders to give you a disclosure called a Loan Estimate within three days of a complete loan application.

The Loan Estimate’s second page shows Points in the top left section called Loan Costs. This will show the exact percentage of the loan amount for any points being quoted. It also shows the dollar amount of the points.

Please note that this Scottsdale Real Estate Blog is for informational purposes and not intended to take the place of a licensed Scottsdale Real Estate Agent. The Szabo Group offers first class real estate services to clients in the Scottsdale Greater Phoenix Metropolitan Area in the buying and selling of Luxury homes in Arizona. Award winning Realtors and Re/MAX top producers and best real estate agent for Luxury Homes in Scottsdale, The Szabo group delivers experience, knowledge, dedication and proven results. Contact Joe Szabo at 480.688.2020, info@ScottsdaleRealEstateTeam.com or visit www.scottsdalerealestateteam.com to find out more about Scottsdale Homes for Sale and Estates for Sale in Scottsdale and to search the Scottsdale MLS for Scottsdale Home Listings.

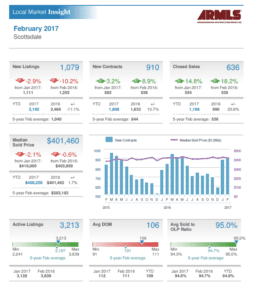

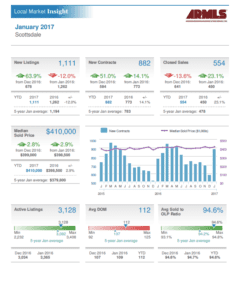

Can you believe it’s already March? The Valley is swarming with snowbirds and sports fans and with all of the poor weather conditions around the country more and more people seem to be eyeing Scottsdale as a possible new home. Let’s take a look at how the Scottsdale real estate market fared in February. New listings are down 2.9% from January with a total of 1,079 new listings vs. 1,111 in January. The new listings in January were driven by homeowners waiting until after the holidays to list their home; it is typical for February numbers to be lower than January for this reason. New contracts and closed sales were both up in February by 3.2% and 14.8% respectively. The median sale is down from $410,000 in January to $401,460 in February. February closed with some motivating numbers – Sellers on the fence are strongly encouraged to take advantage of the low inventory and high demand! During these up and down activity months it is more important than ever to consult a real estate professional that knows the Scottsdale market.

Considering a purchasing or selling a property in Scottsdale? Call Joe and Linda Szabo – The Scottsdale Real Estate Experts!

We hope that you enjoy reading and analyzing the Scottsdale Luxury Home Report and should you have any questions or comments, please feel free to Contact Joe Szabo at 480.688.2020 or email him directly at Joe@ScottsdaleRealEstateTeam.com. You can also visit https://scottsdalerealestateteam.com to find out more about Scottsdale Homes for Sale and Estates for Sale in Scottsdale and to search the Scottsdale MLS for Scottsdale Home Listings.

Please note that this Scottsdale Real Estate Blog is for informational purposes and not intended to take the place of a licensed Scottsdale Real Estate Agent. The Szabo Group offers first class real estate services to clients in the Scottsdale Greater Phoenix Metropolitan Area in the buying and selling of Luxury homes in Arizona. Award winning Realtors and Re/MAX top producers and best real estate agent for Luxury Homes in Scottsdale, The Szabo group delivers experience, knowledge, dedication and proven results.

Can you believe it’s already March? The Valley is swarming with snowbirds and sports fans and with all of the poor weather conditions around the country more and more people seem to be eyeing Scottsdale as a possible new home. Let’s take a look at how the Scottsdale real estate market fared in February. New listings are down 2.9% from January with a total of 1,079 new listings vs. 1,111 in January. The new listings in January were driven by homeowners waiting until after the holidays to list their home; it is typical for February numbers to be lower than January for this reason. New contracts and closed sales were both up in February by 3.2% and 14.8% respectively. The median sale is down from $410,000 in January to $401,460 in February. February closed with some motivating numbers – Sellers on the fence are strongly encouraged to take advantage of the low inventory and high demand! During these up and down activity months it is more important than ever to consult a real estate professional that knows the Scottsdale market.

Considering a purchasing or selling a property in Scottsdale? Call Joe and Linda Szabo – The Scottsdale Real Estate Experts!

We hope that you enjoy reading and analyzing the Scottsdale Luxury Home Report and should you have any questions or comments, please feel free to Contact Joe Szabo at 480.688.2020 or email him directly at Joe@ScottsdaleRealEstateTeam.com. You can also visit https://scottsdalerealestateteam.com to find out more about Scottsdale Homes for Sale and Estates for Sale in Scottsdale and to search the Scottsdale MLS for Scottsdale Home Listings.

Please note that this Scottsdale Real Estate Blog is for informational purposes and not intended to take the place of a licensed Scottsdale Real Estate Agent. The Szabo Group offers first class real estate services to clients in the Scottsdale Greater Phoenix Metropolitan Area in the buying and selling of Luxury homes in Arizona. Award winning Realtors and Re/MAX top producers and best real estate agent for Luxury Homes in Scottsdale, The Szabo group delivers experience, knowledge, dedication and proven results. By

By  The low supply of homes on the market has pushed the ideal window later in the spring. Many shoppers who start searching for a home in early spring may need to look at several homes and make multiple offers, and may still be shopping a few months later.

By May, some buyers will be anxious to avoid more disappointment or eager to get settled into a new home before the next school year — and will be more willing to pay a premium to close the deal.

The May sales boost was particularly notable in Seattle and Portland where sellers who listed in the first half of the month stand to gain the biggest price boost — 2.5 percent in Seattle, 2 percent in Portland — over the area’s average.

On the other end, typically warm weather regions like Miami, Tampa and Phoenix tend show very little variation in sales price or time on market based on listing months. Sellers in these markets will find themselves with more flexibility in choosing when to sell their home.

To apply this analysis to their own home, sellers can use Zillow’s Best Time to List tool to estimate how much listing timing will influence the final sale price in their neighborhood. Registered Zillow users access the tool by clicking the “Sell Your Home” tab on the home details page of their home, and obtain valuable information to pair with the expertise of a local real estate agent when determining the best time to put their home on the market.

The low supply of homes on the market has pushed the ideal window later in the spring. Many shoppers who start searching for a home in early spring may need to look at several homes and make multiple offers, and may still be shopping a few months later.

By May, some buyers will be anxious to avoid more disappointment or eager to get settled into a new home before the next school year — and will be more willing to pay a premium to close the deal.

The May sales boost was particularly notable in Seattle and Portland where sellers who listed in the first half of the month stand to gain the biggest price boost — 2.5 percent in Seattle, 2 percent in Portland — over the area’s average.

On the other end, typically warm weather regions like Miami, Tampa and Phoenix tend show very little variation in sales price or time on market based on listing months. Sellers in these markets will find themselves with more flexibility in choosing when to sell their home.

To apply this analysis to their own home, sellers can use Zillow’s Best Time to List tool to estimate how much listing timing will influence the final sale price in their neighborhood. Registered Zillow users access the tool by clicking the “Sell Your Home” tab on the home details page of their home, and obtain valuable information to pair with the expertise of a local real estate agent when determining the best time to put their home on the market.

By

By  By

By  By

By

If you’re considering to purchase or sell a property in Scottsdale we invite you to reach out to Joe and Linda Szabo with The Szabo Group – The Scottsdale Real Estate Experts! They and their team are more than happy to assist you with any of your real estate needs.

We hope that you enjoy reading and analyzing the Scottsdale Luxury Home Report and should you have any questions or comments, please feel free to Contact Joe Szabo at 480.688.2020 or email him directly at Joe@ScottsdaleRealEstateTeam.com. You can also visit https://scottsdalerealestateteam.com to find out more about Scottsdale Homes for Sale and Estates for Sale in Scottsdale and to search the Scottsdale MLS for Scottsdale Home Listings.

Please note that this Scottsdale Real Estate Blog is for informational purposes and not intended to take the place of a licensed Scottsdale Real Estate Agent. The Szabo Group offers first class real estate services to clients in the Scottsdale Greater Phoenix Metropolitan Area in the buying and selling of Luxury homes in Arizona. Award winning Realtors and Re/MAX top producers and best real estate agent for Luxury Homes in Scottsdale, The Szabo group delivers experience, knowledge, dedication and proven results.

If you’re considering to purchase or sell a property in Scottsdale we invite you to reach out to Joe and Linda Szabo with The Szabo Group – The Scottsdale Real Estate Experts! They and their team are more than happy to assist you with any of your real estate needs.

We hope that you enjoy reading and analyzing the Scottsdale Luxury Home Report and should you have any questions or comments, please feel free to Contact Joe Szabo at 480.688.2020 or email him directly at Joe@ScottsdaleRealEstateTeam.com. You can also visit https://scottsdalerealestateteam.com to find out more about Scottsdale Homes for Sale and Estates for Sale in Scottsdale and to search the Scottsdale MLS for Scottsdale Home Listings.

Please note that this Scottsdale Real Estate Blog is for informational purposes and not intended to take the place of a licensed Scottsdale Real Estate Agent. The Szabo Group offers first class real estate services to clients in the Scottsdale Greater Phoenix Metropolitan Area in the buying and selling of Luxury homes in Arizona. Award winning Realtors and Re/MAX top producers and best real estate agent for Luxury Homes in Scottsdale, The Szabo group delivers experience, knowledge, dedication and proven results. By

By