We at Scottdale Real Estate Team off your best wishes for a wonderful holiday season and a new year filled with peace, prosperity and happiness. Happy holidays and a very happy 2018!

We at Scottdale Real Estate Team off your best wishes for a wonderful holiday season and a new year filled with peace, prosperity and happiness. Happy holidays and a very happy 2018!

Happy Holidays from Joe Szabo & the Scottsdale Real Estate Team

We at Scottdale Real Estate Team off your best wishes for a wonderful holiday season and a new year filled with peace, prosperity and happiness. Happy holidays and a very happy 2018!

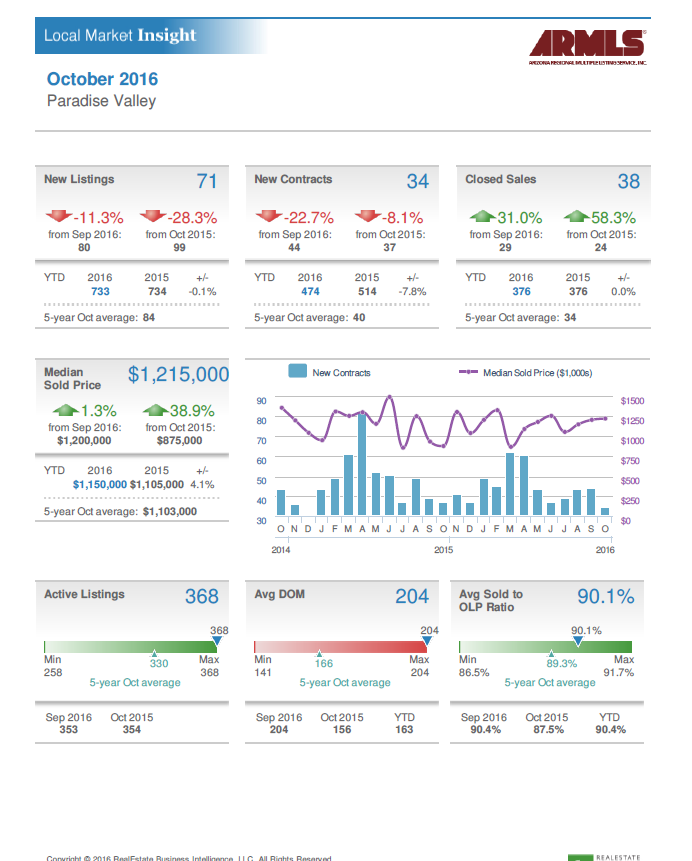

Can you believe it’s already February? Let’s take a look at how the Paradise Valley real estate market faired in January. New listings are up by 65.4% from December with a total of 86 new listings vs. 52 in December. The new listings in January were driven by homeowners waiting until after the holidays to list their home. New contracts were up in January by 38.9% with 50 new listings and closed sales went up with January numbers at 36 closed sales vs. 33 in December. The median sale is down from $1,104,000 in December to $983,750 in January. January closed with some motivating numbers – Sellers on the fence are strongly encouraged to take advantage of the low inventory and high demand! . During these up and down activity months it is more important than ever to consult a real estate professional that knows the Paradise Valley market.

If you’re considering to purchase or sell a property in Scottsdale we invite you to reach out to Joe and Linda Szabo with The Szabo Group – The Scottsdale Real Estate Experts! They and their team are more than happy to assist you with any of your real estate needs.

We hope that you enjoy reading and analyzing the Paradise Valley Luxury Home Report and should you have any questions or comments, please feel free to Contact Joe Szabo at 480.688.2020 or email him directly at

Can you believe it’s already February? Let’s take a look at how the Paradise Valley real estate market faired in January. New listings are up by 65.4% from December with a total of 86 new listings vs. 52 in December. The new listings in January were driven by homeowners waiting until after the holidays to list their home. New contracts were up in January by 38.9% with 50 new listings and closed sales went up with January numbers at 36 closed sales vs. 33 in December. The median sale is down from $1,104,000 in December to $983,750 in January. January closed with some motivating numbers – Sellers on the fence are strongly encouraged to take advantage of the low inventory and high demand! . During these up and down activity months it is more important than ever to consult a real estate professional that knows the Paradise Valley market.

If you’re considering to purchase or sell a property in Scottsdale we invite you to reach out to Joe and Linda Szabo with The Szabo Group – The Scottsdale Real Estate Experts! They and their team are more than happy to assist you with any of your real estate needs.

We hope that you enjoy reading and analyzing the Paradise Valley Luxury Home Report and should you have any questions or comments, please feel free to Contact Joe Szabo at 480.688.2020 or email him directly at

By

By

cleaned and stored. Check hoses for cracks, holes or other faults, store propane tanks away from your home if you have a gas grill, don’t cover or put away your grill until it has cooled, rinse charcoal with cool water before disposing of it, and keep a fire extinguisher nearby. Don’t grill in an enclosed area.

While grownups man the grill, kids may choose to jump around on the trampoline. Nearly 105,000 children visited emergency rooms last year for injuries caused by trampolines, according to the Consumer Product Safety Commission.

To prevent injuries, don’t take shortcuts when assembling the trampoline. Furthermore, pad the bars, springs and the surrounding areas, and get the trampoline as close to ground level as possible to reduce potential impact if a jumper falls.

Always supervise trampoline use, and let your insurance provider know about this type of addition to your home. You need a fence around it for the same reason you need one around a swimming pool on your property.

cleaned and stored. Check hoses for cracks, holes or other faults, store propane tanks away from your home if you have a gas grill, don’t cover or put away your grill until it has cooled, rinse charcoal with cool water before disposing of it, and keep a fire extinguisher nearby. Don’t grill in an enclosed area.

While grownups man the grill, kids may choose to jump around on the trampoline. Nearly 105,000 children visited emergency rooms last year for injuries caused by trampolines, according to the Consumer Product Safety Commission.

To prevent injuries, don’t take shortcuts when assembling the trampoline. Furthermore, pad the bars, springs and the surrounding areas, and get the trampoline as close to ground level as possible to reduce potential impact if a jumper falls.

Always supervise trampoline use, and let your insurance provider know about this type of addition to your home. You need a fence around it for the same reason you need one around a swimming pool on your property.